Explore More Possibilities for Your Business

Full-cycle scenario construction to meet your needs from App research, development, and release to operation.

Ready for your soaring growth

The global retail industry is once again approaching the annual Black Friday shopping season.

FoxData has also prepared some exciting special offers for you. But before that, let’s look back at the performance of the app market during Black Friday 2024 — insights that may inspire this year’s promotional strategies.

According to PYMNTS Intelligence’s research, Black Friday remains the core of holiday shopping, with 43% of total holiday budgets spent during Black Friday discounts. However, 39% of Black Friday spending actually occurred before the day itself, indicating that the consumption cycle for this event has continued to extend forward.

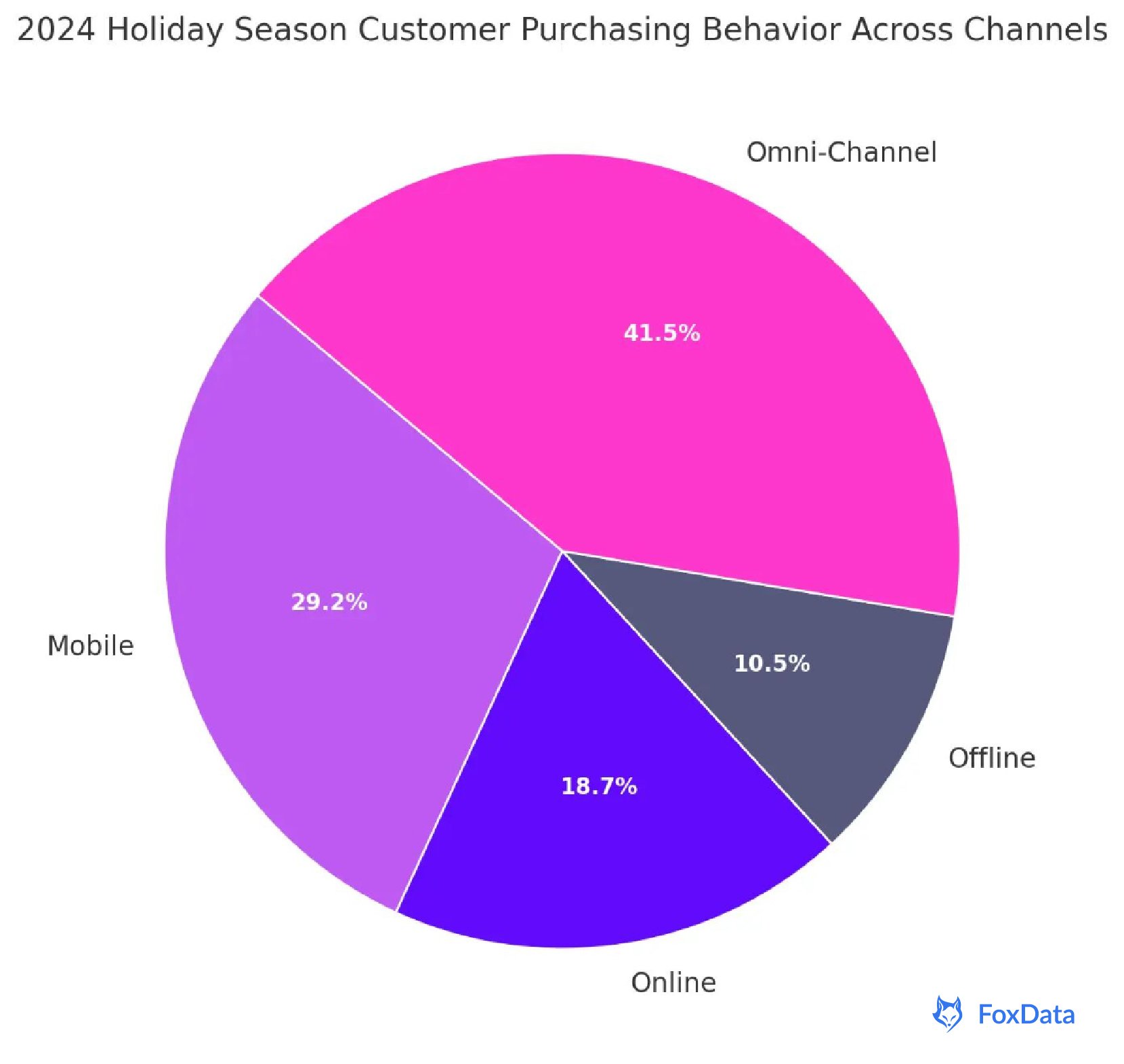

Compared with previous years, Black Friday 2024 showed a clear structural shift: offline sales stabilized while online channels surged comprehensively.

According to Mastercard and various research agencies, U.S. retail store sales saw only limited growth, while e-commerce sales recorded double-digit increases, reaching an all-time high. Behind this trend, inflation has driven consumers to become more price-sensitive, while aggressive discount campaigns and transparent price comparisons across e-commerce platforms have made “value-for-money shopping” the dominant mindset.

From a category perspective, toys, electronics, and home appliances have become the main drivers of online growth, whereas traditionally stable verticals such as health and beauty saw rare declines. Factors such as lower foot traffic in physical stores, regional weather fluctuations, and more fragmented purchasing behaviors are collectively redefining the boundaries of “Black Friday.”

Meanwhile, e-commerce giants such as Amazon and Walmart continued to dominate the market, while emerging players including SHEIN, Temu, and TikTok Shop delivered strong performances throughout the period — collectively intensifying digital retail competition.

For brands and developers, Black Friday is no longer merely a sales arena but has evolved into a testing ground for data insights and user growth strategies.

Against this backdrop, FoxData looks back on the performance of the app market during Black Friday 2024 — breaking down growth signals across downloads, user activity, marketing strategies, and consumer psychology — to provide practical insight and strategic guidance for the coming holiday cycle.

A multi-core growth pattern is emerging: iOS user acquisition is no longer monopolized by a single e-commerce app. Platforms such as Whatnot (live shopping + social) and Shop (Shopify’s merchant ecosystem) are jointly driving a dual-track growth model of “contentization + toolization.” This shift signifies a broader change in e-commerce dynamics — from platform-driven to scenario-driven growth, where users may discover products through live streams and complete purchases on independent websites.

High-trust ecosystems reinforce brand moats: iOS users tend to have higher purchasing power and brand sensitivity, making complete shopping experiences — secure payments, transparent logistics, and responsive after-sales — critical to loyalty.

Consequently, Amazon, Walmart, and Target continue to dominate top traffic positions. These brands rely on mature membership systems and robust data assets to create LTV (lifetime value)-driven growth loops.

Temu + SHEIN: The “two Chinese powerhouses” enter their second stage of competition: Both have evolved beyond “subsidy-driven growth” toward a more balanced game of brand perception + supply chain agility.

💡 Extended Insight:

E-commerce on iOS has shifted from a traffic competition to a contest of experience and user trust. This reflects the growing preference among upper-tier Western consumers for brand reliability and service certainty, which will increasingly determine profit margins in future Black Friday seasons.

Temu’s “mass adoption” accelerates across Android: Both downloads and DAU outperform its iOS metrics, indicating that Android ecosystems host more impulse-driven and price-sensitive user groups. Through fast-loading ad creatives and referral-based cashback programs, Temu achieves low-cost user acquisition — representing algorithmic, data-driven growth rather than pure brand pull.

The Amazon–Walmart gap narrows as “local service experience” emerges as the key differentiator:

Android users display stronger reliance on features such as one-click pickup, same-day delivery, and cumulative membership discounts. While Amazon enjoys strong brand recognition, Walmart leverages its extensive store network to gain deeper regional market penetration.

As the focus shifts from “price” to “efficiency,” large local retailers are redefining user loyalty within the mobile ecosystem.

AliExpress + Alibaba.com dual-platform synergy illustrates a closed-loop supply chain cycle:

💡 Observation:

Influenced by China’s “Double 11” campaigns and massive user bases, Chinese shopping apps still occupy a significant share of global rankings, underscoring their strong global penetration and inherent advantages in pricing, supply chain integration, and cross-border fulfillment.

1️⃣ Amazon: The unshakable leader with structural traffic and conversion strength

Amazon reached a Black Friday peak of approximately 20.21M DAU (iOS) / 3.6M DAU (Android), remaining at a high plateau with minimal drop-off.

2️⃣ Temu: Post-event resilience and gradual retention maturity

Temu’s DAU increased from 1.1M to 1.5M and remained steady into early December, showing post-event retention robustness.

3️⃣ SHEIN & AliExpress: Typical “promotion-peak” patterns with limited post-event loyalty

Both recorded strong spikes around Black Friday but declined sharply in early December, forming a pulse-shaped activity curve.

4️⃣ Alibaba.com (1688 Global): Distinct B-end resurgence reveals supply chain value

While most consumer apps saw declines, Alibaba.com’s DAU rose to ~360K at month-end.

Black Friday 2024 highlighted a clear turn toward data-centric and experience-oriented marketing.

Retailers are no longer relying solely on deep discounts but instead executing omnichannel, personalized, and interactive content experiences.

Most brands adopted a three-phase strategy: early warming-up, real-time engagement, and extended promotions, integrating social buzz, live streaming, and in-app messages to sustain a continuous festive atmosphere.

Simultaneously, content marketing and influencer collaborations became decisive levers. Through partnerships with creators on TikTok, Instagram, and other platforms, brands translated viral engagement into conversions, completing the “content-to-commerce” loop.

With purchase paths becoming increasingly fragmented and decision cycles shorter, real-time engagement capability now directly determines conversion efficiency.

In addition, retailers increasingly rely on data-driven marketing automation and AI-powered recommendation systems to optimize audience targeting, behavioral analytics, and advertising ROI — adopting smarter, performance-led marketing models.

In short, Black Friday is no longer a discount war — it has evolved into a competition driven by data, content, and technology.

Under persistent economic uncertainty, price sensitivity and self-rewarding consumption have emerged as defining traits. Confronted with inflation and rising living costs, consumers are spending more on “gifts for themselves” that bring instant satisfaction rather than on traditional giving.

This “instant gratification” mindset signals a structural pivot — from gift-oriented to self-reward shopping behaviors, reshaping engagement strategies.

While the biggest discounts remain the prime motivation, spending is still concentrated in discretionary categories. Moreover, “Buy Now, Pay Later” (BNPL) users spent more than credit or debit card users; according to PYMNTS Intelligence, financially stable BNPL users outspent peers using conventional payment by as much as 86%.

At the same time, brand loyalty is being redefined. With tighter budgets, consumers are more willing to switch to competitively priced alternatives — loyalty is no longer a given. To win back user trust and stickiness, brands must focus on real value perception and frictionless, enjoyable digital experiences.

Black Friday 2024 reaffirmed the acceleration toward digitalization, intelligence, and experience-driven retail.

The sustained rise of online channels, evolving consumer psychology, and deep integration of AI and content-based marketing are systematically reshaping how brands engage with users.

For both e-commerce platforms and app developers, data intelligence has become the essential weapon against uncertainty and a key enabler for capturing growth opportunities.

⚠️ Black Friday 2025 will be even more competitive — Temu’s sale period extends nearly a month, TikTok Shop doubles exposure for managed sellers, and Amazon’s “Green Label” items earn 18% higher conversion rates.

Every moment of delayed analysis means missing a traffic peak.

👉 Now is the time to act — accelerate with data-driven decisions and seize the momentum for Black Friday 2025!

This year, FoxData’s limited-time Black Friday offers are coming soon!

Start your free trial today to experience data-powered marketing efficiency. Once the campaign launches, you’ll unlock full-featured plans at exclusive prices — empowering your brand to reach new highs this Black Friday.

✨ Want to spot trends earlier and capture opportunities before others?

Register now and get ahead of the competition with FoxData — win the race to insight!

© 2020-2026 FoxData. All Rights Reserved.