Explore More Possibilities for Your Business

Full-cycle scenario construction to meet your needs from App research, development, and release to operation.

Ready for your soaring growth

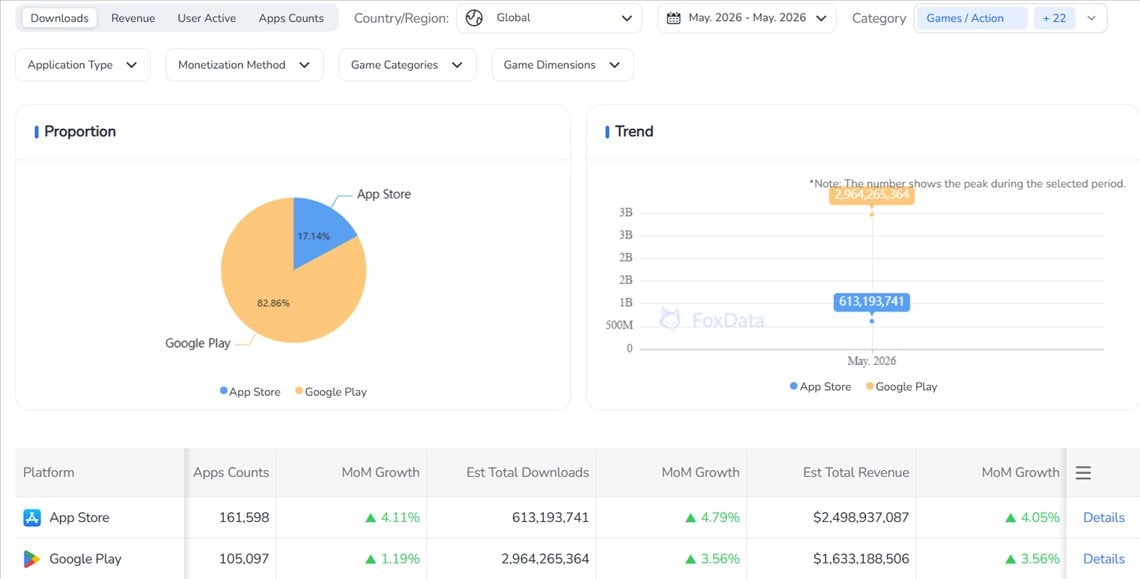

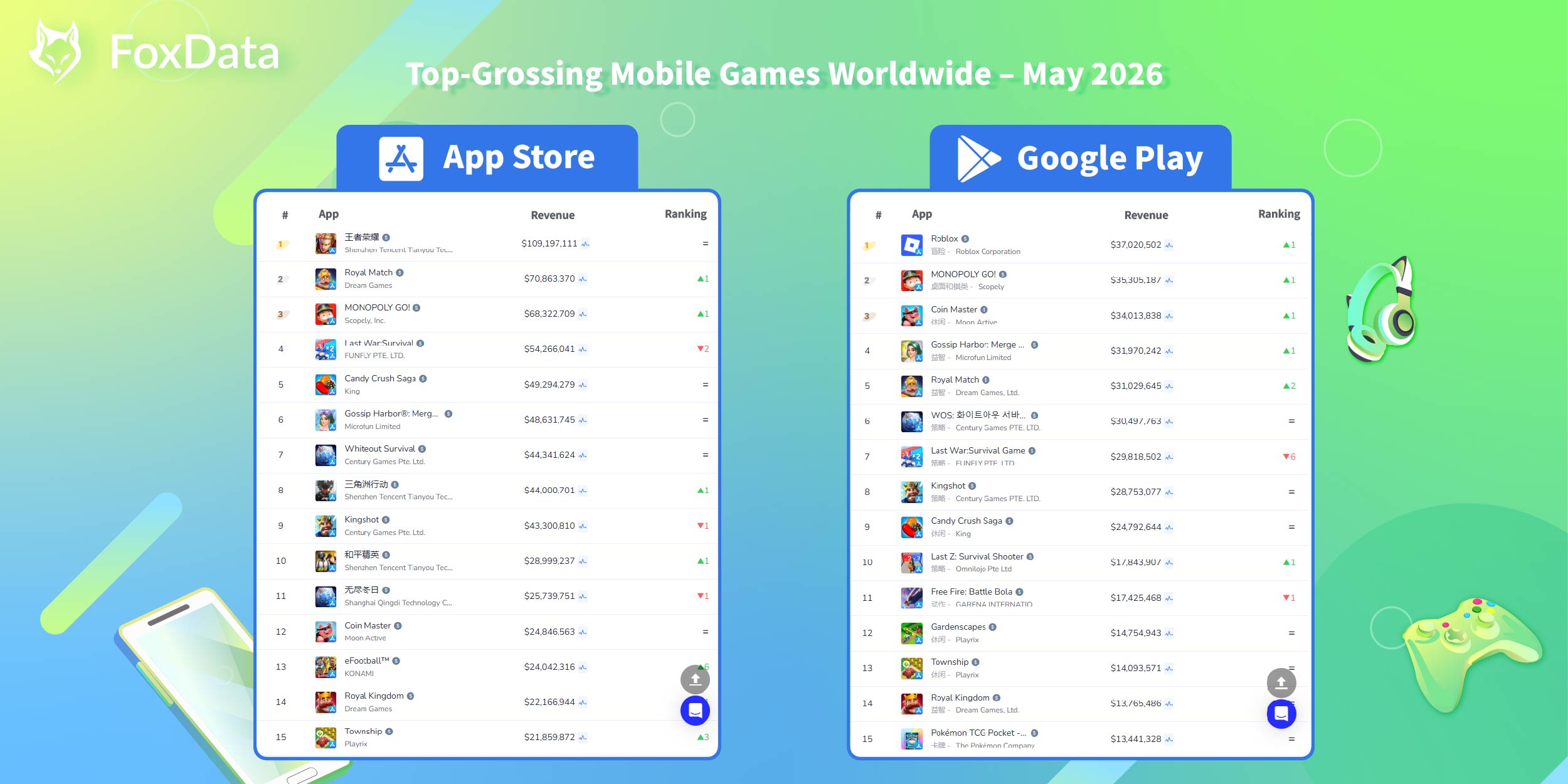

Data Period: May 1–31, 2026

Data Source: FoxData Download & Revenue Rankings

Platforms: App Store & Google Play

Geographic Scope: Global

May 2026 was a strong month for mobile games. Downloads and revenue both increased — a rare combination and a positive signal for the industry.

But the growth wasn't evenly shared. As Summer Game Fest, the PlayStation Showcase, and Xbox Games Showcase drew core gamers toward console and PC titles, casual and mid-core mobile games seized the opportunity. At the same time, anniversary events from Wuthering Waves, Honkai: Star Rail, and School Idol: Uta no Prince-sama fueled an anime game resurgence in Japan, while NTE: Neverness to Everness emerged as a breakout hit with nearly $17 million in overseas revenue.

The 2026 FIFA World Cup also began casting its shadow over the market. Soccer games ramped up UA spending, and Konami successfully turned eFootball's anniversary campaign into a pre-tournament growth engine.

According to FoxData, downloads grew 4.33% MoM and 24.2% YoY in May, while revenue rose 2.94% MoM and 7.1% YoY.

Source: FoxData-App Market Intelligence

Beneath those headline numbers, however, the market is shifting. Top performers are consolidating, legacy SLG games are quietly losing ground, and lightweight casual titles are climbing the charts through increasingly efficient user acquisition.

May's rankings are more than a leaderboard update — they're a snapshot of where the mobile gaming market is headed.

💡 The numbers tell you what happened. FoxData tells you why — and what's next.

Track download-revenue divergence, publisher momentum shifts, and category-level trend signals across every major market.

Explore FoxData Mobile Game Analytics →

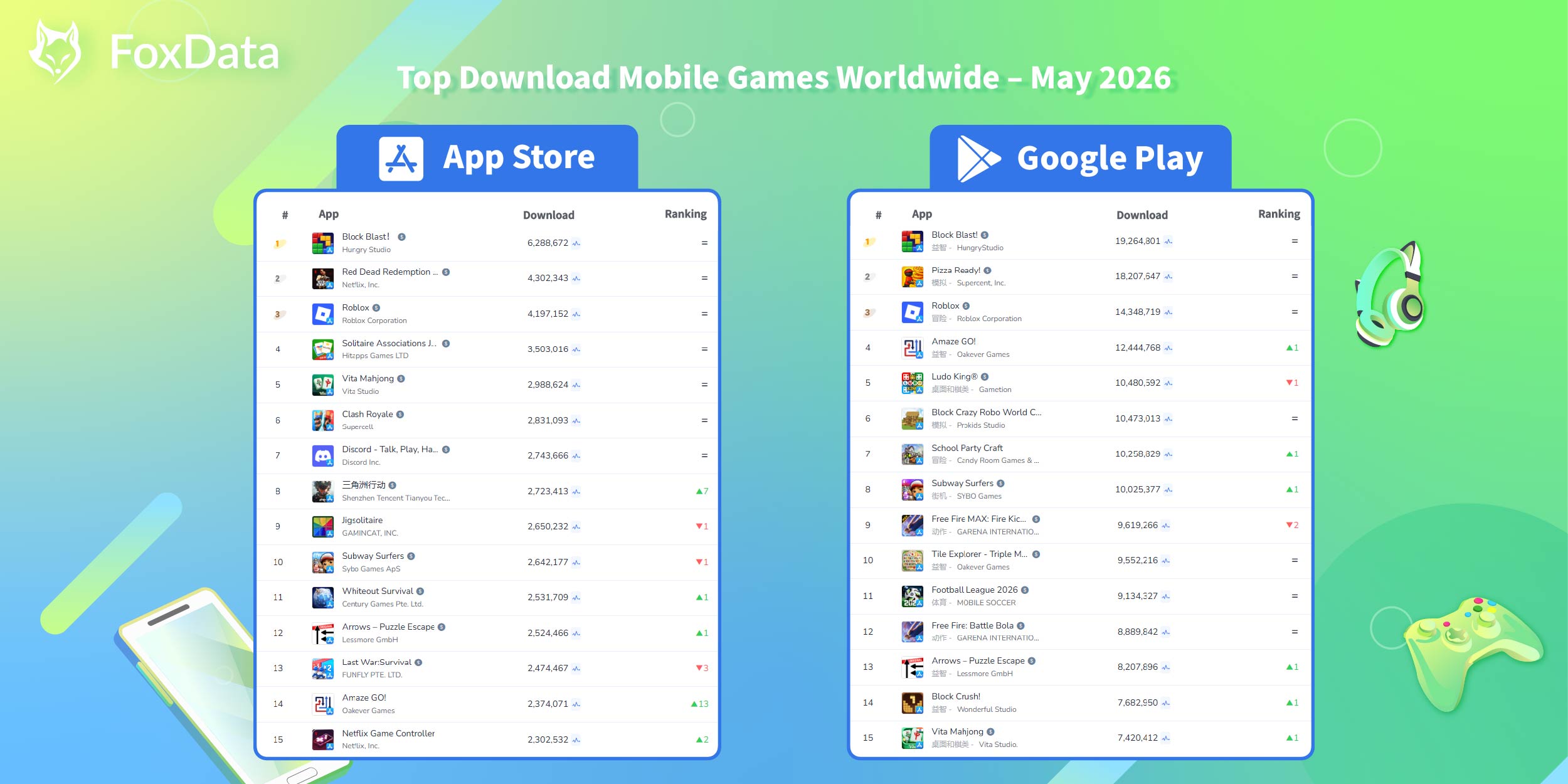

Data source: FoxData Download Charts

May 2026 App Store download rankings were dominated by casual puzzle titles and hybrid-casual games, with notable movement from sports simulation titles driven by World Cup-related content events.

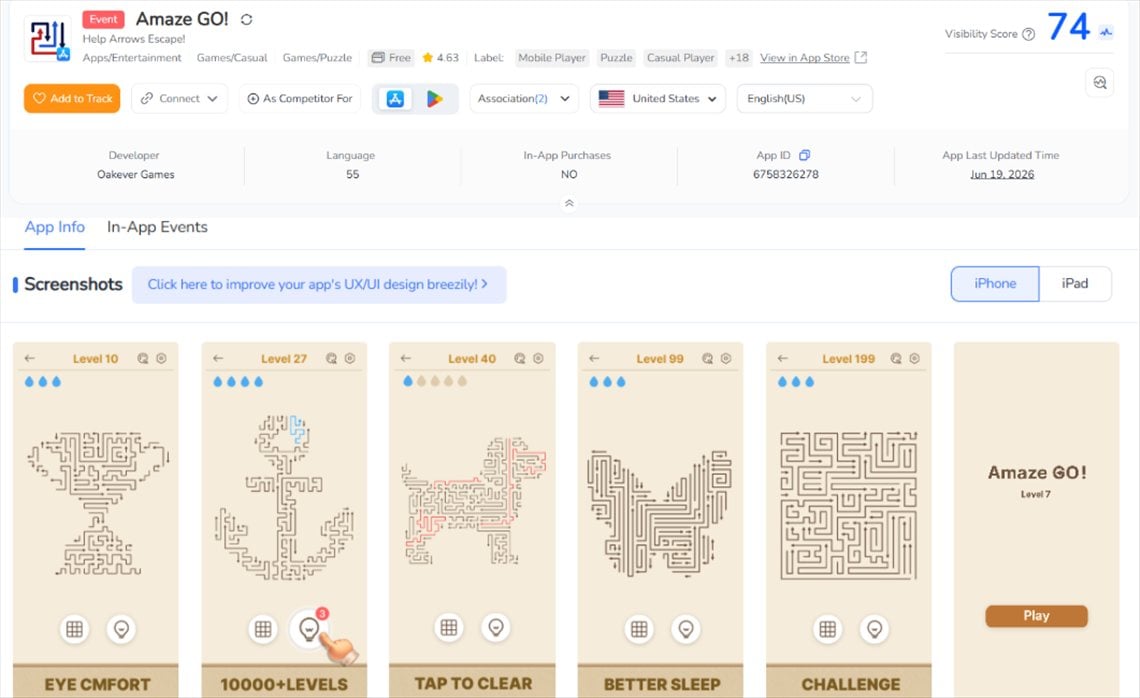

Amaze GO! — up 13 positions

Thirteen spots in a single month is an outlier on any platform. Amaze GO! is a casual puzzle game — dead-simple mechanics, instant visual payoff, designed for five-minute sessions. It follows the exact same playbook as April's breakout Jewel Coloring: zero learning curve, maximum shareability, frictionless everything.

The game had been live since 2025 without making much noise. Then came a heavy UA push in April and May — and downloads spiked to an all-time high since launch.

The engine driving it? Short-form video. On TikTok and Instagram Reels, Amaze GO!'s arrow-guidance gameplay is self-explanatory in under three seconds. Viewers understand the rules before the clip ends. That "needs no explanation" quality makes paid creative extraordinarily efficient — and almost impossible to replicate with traditional ad formats.

Delta Force — up 7 positions

Tencent's tactical shooter had a natural tailwind from Labor Day Golden Week in early May, which reliably pulls back lapsed players. But the real lift came later: a crossover with the Jingdezhen Imperial Kiln Institute, one of China's most iconic cultural heritage institutions.

The "Delta Force × Jingdezhen Imperial Kiln Institute" campaign wove traditional porcelain aesthetics into the game's visual identity — giving a military shooter a cultural narrative it had no business having, and pulling in audiences well outside its core base. Downloads responded visibly. It's a clean example of how the right cultural IP partnership can function as UA in its own right.

📌 The key takeaway for game publishers is simple: pick a lane. In today's mobile gaming market, trying to be both lightweight and heavyweight is rarely a winning strategy.

🔍 Tracking which casual titles are breaking out — and why — before they hit the top 15?

See what's moving before it's obvious →

Unlike the App Store, where breakout hits fueled major movement, the global Google Play download rankings in May was defined by stability. Nearly every title moved by just one or two positions, reflecting a far more cautious market.

That alone was an improvement from April, when several games suffered sharper declines. The broader sense of downward pressure had largely faded.

Part of the recovery came from rising traffic ahead of the 2026 World Cup, while several mid-core launches also brought fresh users into the ecosystem. Together, these factors helped keep Android downloads stable, even if growth remained muted.

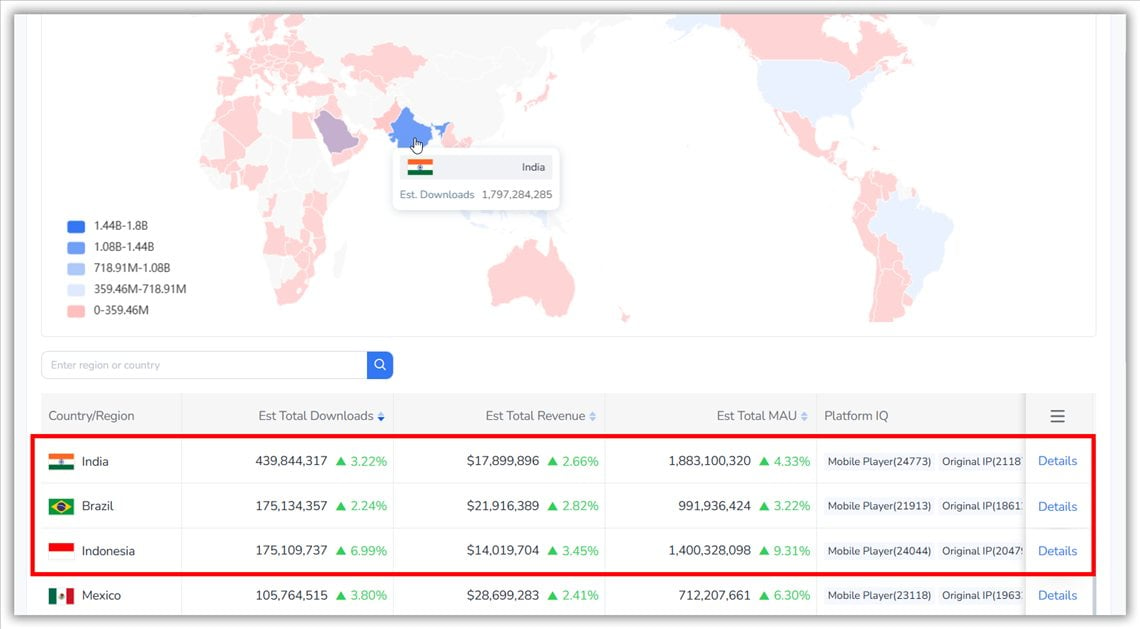

Behind the stable rankings, emerging markets continue to drive Android downloads.

According to FoxData-App Market Intelligence, India, Brazil, and Indonesia remained the biggest contributors to Google Play download growth. However, stronger downloads in these markets don't always translate into higher revenue.

This highlights the growing difference between iOS and Android strategies:

For global publishers, a differentiated approach is becoming essential: use aggressive user acquisition on iOS, while focusing on long-term brand building and localization on Android.

🚀 The next wave of mobile growth is happening in emerging markets.

FoxData monitors download trends across 50+ countries, uncovering early signals from India, Brazil, Indonesia, and other high-growth regions before they become mainstream.

Explore market-level intelligence on FoxData →

Data source: FoxData Revenue Charts

May delivered the most dynamic App Store revenue chart in months.

After April's unusually stable rankings, May brought renewed momentum. Games that gained ground climbed between 1 and 6 positions, while those that slipped fell by just 1–2 spots. More room to rise and less room to fall—that's what a healthy, expanding market looks like.

The pattern reflects the broader industry trend. With the global mobile game market growing 7.1% year over year in May, the App Store leaderboard wasn't being reshuffled—it was growing.

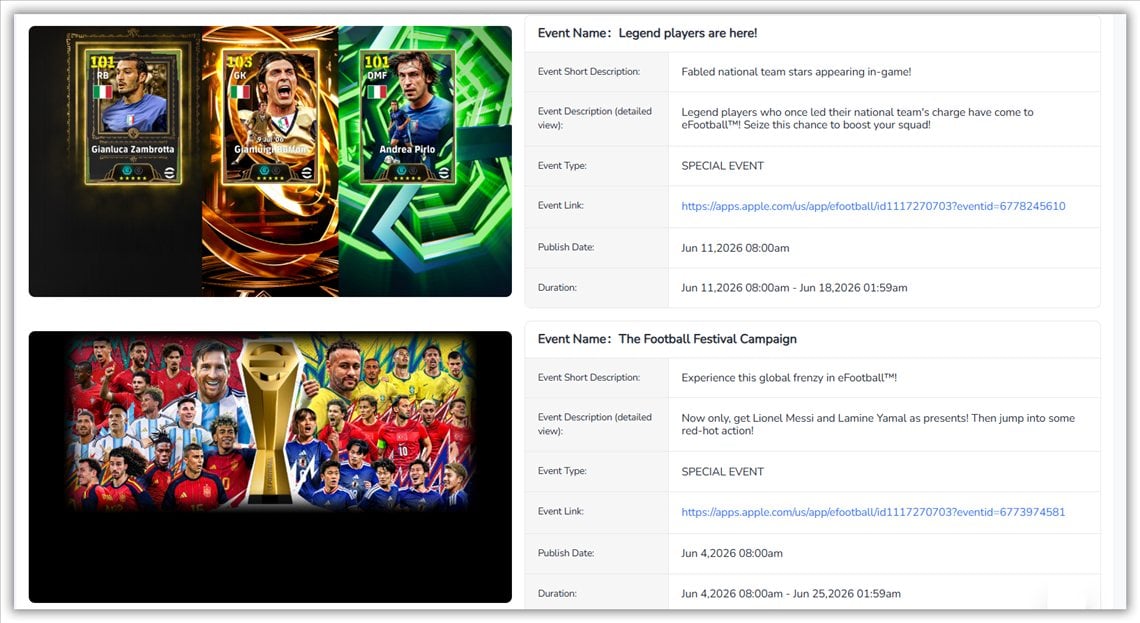

The Standout Mover: eFootball™ (up 6 positions)

After jumping 12 places in April, eFootball™ climbed another six spots in May. Back-to-back gains like this are no accident.

Konami activated two growth drivers at the same time. The first was the game’s Mobile 9th Anniversary. Mid-May events, limited-time content, and comeback campaigns lifted DAU by 12.7%, bringing lapsed players back.

The second was World Cup anticipation. As the 2026 FIFA World Cup approached its June 11 kickoff, football hype naturally spilled into gaming, turning player-card spending into part of the fan experience.

Source: eFootball™ In-App Events

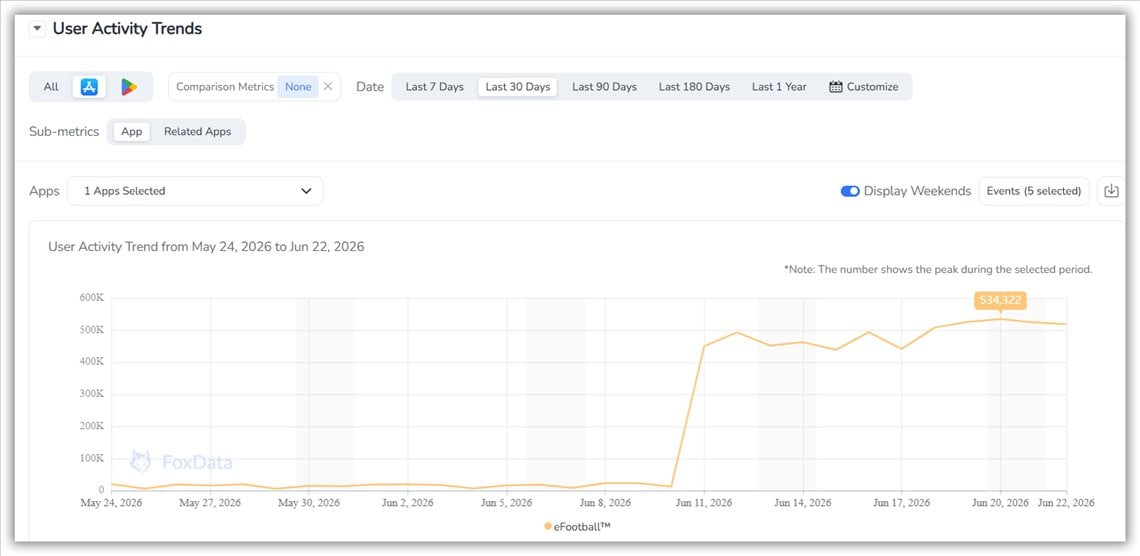

FoxData Intelligence shows eFootball™ ranked No. 1 in Japan by revenue in May. Revenue was down just 1.3% month over month, while DAU rose 12.7%—a classic pre-monetization signal. The audience grew first, with spending likely to follow.

Source: FoxData Active Users Analysis — eFootball™ (Japan)

Anniversary nostalgia, World Cup momentum, and limited-time legendary players all reinforced each other, making the six-position climb a clear result of strong live ops execution.

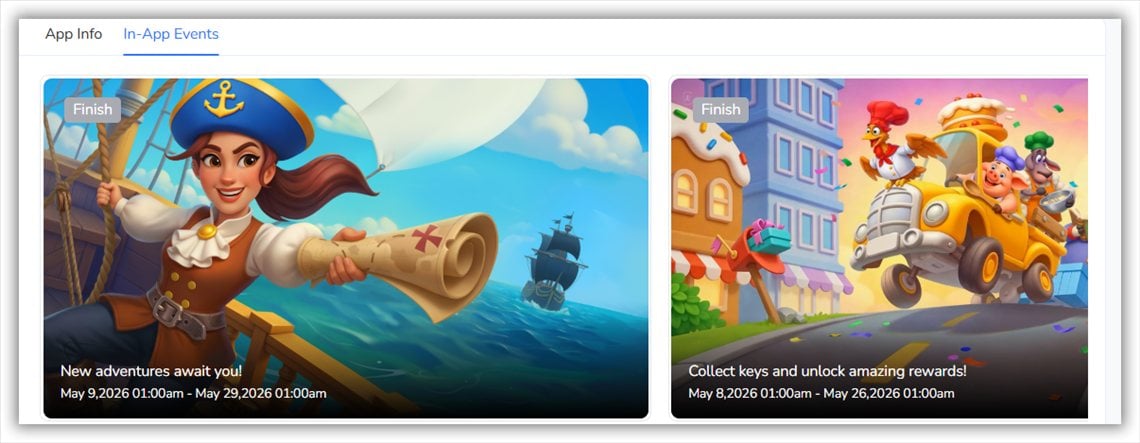

The Quiet Performer: Township (up 3 positions)

eFootball™ grabbed the headlines. Township made quieter— but equally meaningful —progress.

Playrix's simulation-puzzle title climbed three spots in May through a very different playbook: strong seasonal live ops. Early-summer events and new building content arrived at just the right point in the calendar, and Township's loyal players responded with their wallets.

Source: Township In-App Events

🔍 Event-driven revenue spikes are predictable — if you know where to look.

FoxData tracks DAU trends, revenue momentum, and live-ops timing patterns across the top grossing charts, so your team can benchmark competitors' event strategies before they execute them.

Track event-driven revenue signals on FoxData →

May's Google Play revenue chart closely mirrored the download rankings: stable, orderly, and largely predictable—until one title broke away from the pack.

Most games moved just 1–2 positions in either direction. Golden Week traffic, rising World Cup excitement, and a packed anniversary event calendar kept Android revenue flowing steadily throughout the month. Gains were controlled, and so were losses.

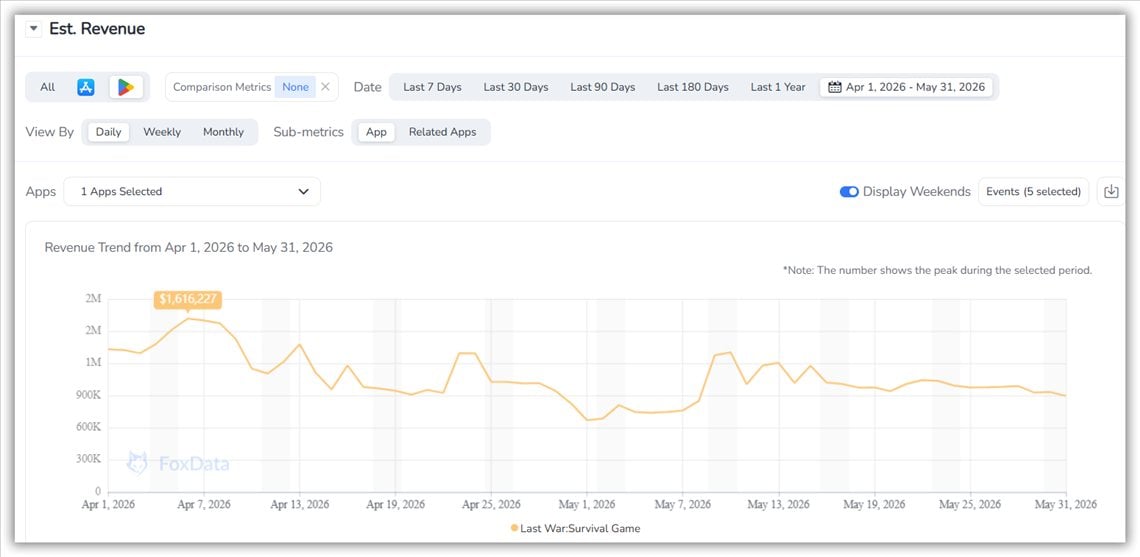

The Biggest Drop: Last War: Survival (-6)

A six-position decline in a chart where almost nothing moved more than two spots was impossible to ignore.

According to FoxData, Last War: Survival saw revenue fall 26.0% MoM, while downloads plunged 72.9% and DAU declined 9.9%.

When revenue, installs, and daily engagement all decline at the same time, it's more than a slow month between updates. It's a sign that deeper structural pressure is beginning to show.

Whiteout Survival revealed a similar pattern worth watching. Revenue edged up 2.6% month over month, but downloads fell 72.9%. At first glance, stable revenue alongside collapsing installs may look like improving monetization efficiency. In SLG, however, it often signals something else: existing whales are still spending, but the pipeline of new players is starting to dry up.

SLG monetization runs on competition.

Alliance wars, resource battles, and server rankings give players a reason to spend. The desire to win only matters when there are opponents worth beating.

As player populations shrink, that competitive intensity starts to fade. Alliances weaken, servers become quieter, and the urgency to spend diminishes. Top spenders rarely disappear overnight, but their motivation gradually erodes—and revenue tends to follow with a lag.

This creates the classic SLG death spiral:

Players leave → competition weakens → spending declines → more players leave.

Each stage reinforces the next. By the time revenue shows meaningful damage, the underlying player ecosystem has often been deteriorating for weeks—sometimes months.

Genre fatigue can make the problem even worse. Once the appeal of a particular SLG theme begins to fade, user interest can decline faster than operators expect—and faster than retention tools can offset.

Four themes defined the global mobile game market in May 2026:

Chinese publishers accounted for 38 of the global top 100 publishers by revenue in May, generating a combined $2.29 billion and capturing 42.8% of Top 100 revenue—up 6.2 percentage points year over year.

Behind those numbers were standout performances from Tencent, HoYoverse, Kuro Games, and Perfect World. More importantly, they reflected years of investment in quality, live operations, and global distribution.

Chinese mobile gaming is no longer chasing the market. It's leading it.

May saw strong performances from Ananta, Wuthering Waves, and Honkai: Star Rail.

Three major anime titles generating momentum at the same time signals something bigger than individual success. The genre itself is entering its most competitive summer yet, with higher expectations—and higher revenue potential—than ever before.

The 2026 FIFA World Cup is the biggest event window soccer games will see for the next four years. Titles like eFootball™ and EA SPORTS FC™ Mobile have already started benefiting from rising football interest. June will reveal how much of that momentum translates into revenue.

The end of China's college entrance exams consistently drives a surge in downloads and new-user acquisition. Casual and anime titles are particularly well positioned to benefit from this seasonal demand.

Major releases and post-launch updates across anime, SLG, and MOBA categories will make June and July increasingly competitive. Protecting core users while fighting for attention will become a key challenge for publishers.

As AI-powered creative tools become more accessible, smaller teams are gaining the ability to compete with established studios. Summer 2026 could produce more surprise hits than usual.

May highlighted both the strength of today's market leaders and the new trends reshaping the industry. The next 60 days will show which publishers can sustain their momentum—and which ones can't.

FoxData delivers cross-platform game intelligence for publishers, UA teams, and investors, helping them track competitors, uncover trends, and make smarter decisions across mobile, Steam, and console.

© 2020-2026 FoxData. All Rights Reserved.