Explore More Possibilities for Your Business

Full-cycle scenario construction to meet your needs from App research, development, and release to operation.

Ready for your soaring growth

Recently, the European mobile gaming industry received its first comprehensive economic impact study - Mobile Matters: The Impact of Mobile Games for Europe - commissioned by a coalition of industry stakeholders and produced by international consulting firm Nordicity. The findings confirm what many in the ecosystem have long understood: mobile gaming is a heavyweight economic sector, not a niche entertainment vertical.

The numbers are unmistakable:

📱 European mobile game companies generated an estimated €7.53 billion in global revenue

💶 The industry contributed approximately €5.89 billion in Gross Value Added (GVA) to the European economy

👥 The sector directly and indirectly supports 63,000+ jobs across more than 1,000 studios region-wide

📊 Mobile gaming now accounts for 55% of all video games revenue worldwide

🌍 More than 300 million people in Europe play mobile games - representing 61% of the continent's population, with the average player aged 31 and 75% of the player base being adults

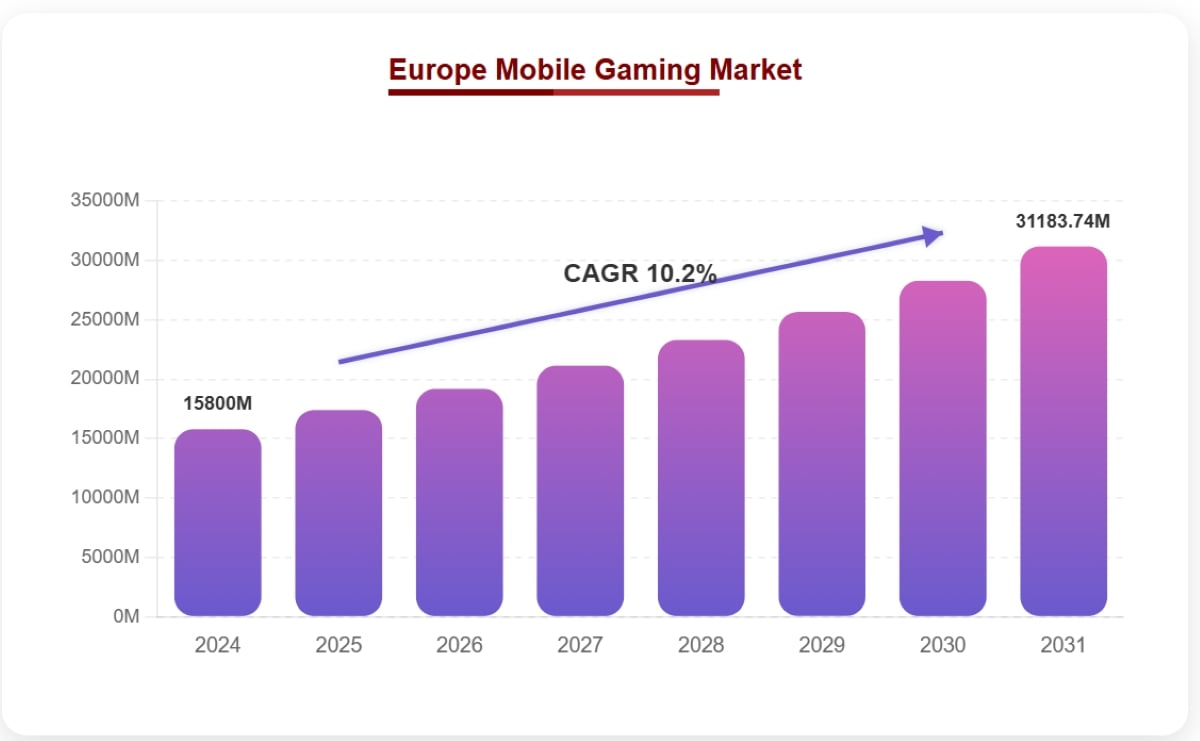

mobile games Europe revenue | Source from Intel Market Research

Industry leaders are now calling on policymakers to treat mobile gaming as a strategic growth engine deserving dedicated infrastructure and talent investment. For game developers, publishers, and marketers operating in or eyeing the European market, this report is more than a headline - it's a strategic signal. Below, we break down what the data tells us, why it matters for growth strategy, and how data-driven tools can help you capture your share of this expanding market.

📊 FoxData Perspective: The €5.89 billion GVA figure matters strategically because it quantifies what we observe daily in our platform data - European mobile gaming is not merely growing; it is structurally diversifying. Our app intelligence data shows that Europe's top-grossing markets are increasingly driven by mid-core and strategy titles alongside the casual mainstays, creating multiple parallel revenue streams that reinforce the continent's resilience as a development hub. Independent market research from Intel Market Research corroborates this trajectory, valuing the European mobile gaming market at USD 15.8 billion in 2024 with projections to reach USD 28.4 billion by 2030 - a 10.2% CAGR.

One of the most important distinctions in the data is the difference between revenue and economic contribution:

| Metric | Figure |

|---|---|

| Global revenue generated by European mobile game companies | €7.53 billion |

| Economic value (GVA) contributed to Europe | €5.89 billion |

| Jobs supported (direct + indirect) | 63,000+ |

| Active studios across the region | 1,000+ |

| Projected European GDP contribution by 2028 | €6.17 billion |

| Projected global revenues by 2028 | >€8 billion |

The €5.89 billion GVA figure accounts for the multiplier effect - wages paid to developers, designers, and marketers; spending by those employees in local economies; investment into tech infrastructure; and taxes generated for EU member states. This is the figure that makes policymakers take notice.

📊 FoxData Perspective: The projected trajectory from €5.89 billion to €6.17 billion by 2028 signals steady rather than explosive near-term growth in economic contribution. However, our platform data across both the App Store and Google Play suggests that revenue concentration is intensifying - the top 5% of titles capture an increasing share of total European market revenue. This means market entry is getting harder for undifferentiated products while getting more rewarding for data-informed launches. Separately, Intel Market Research data indicates in-app purchases account for approximately 65% of total European mobile gaming spending - making IAP optimization the single highest-leverage monetization lever available to developers targeting the region.

Why this matters for developers: When an industry demonstrates economic multiplier effects at this scale, it typically attracts favorable policy environments — including grants, tax incentives, and R&D credits. European mobile developers should be positioning to take advantage.

The Nordicity study identifies clear revenue concentration across Europe's major development hubs, with country-level GVA figures revealing the competitive landscape

| Country | Estimated Industry Revenue |

|---|---|

| 🇫🇮 Finland | €1.4 billion |

| 🇬🇧 United Kingdom | €895 million |

| 🇮🇪 Ireland | €868 million |

| 🇪🇸 Spain | €722 million |

| 🇸🇪 Sweden | €630 million |

Additional key markets shaping the landscape:

🇩🇪 Germany - Largest consumer market within the EU, strong publishing ecosystem

🇫🇷 France - Strong in mid-core publishing and home to Ubisoft Mobile's European operations

🇬🇧 United Kingdom - Historically Europe's largest games market; our recent breakdown of the PocketGamer Top 50 UK Game Makers 2026 covers the competitive landscape in detail

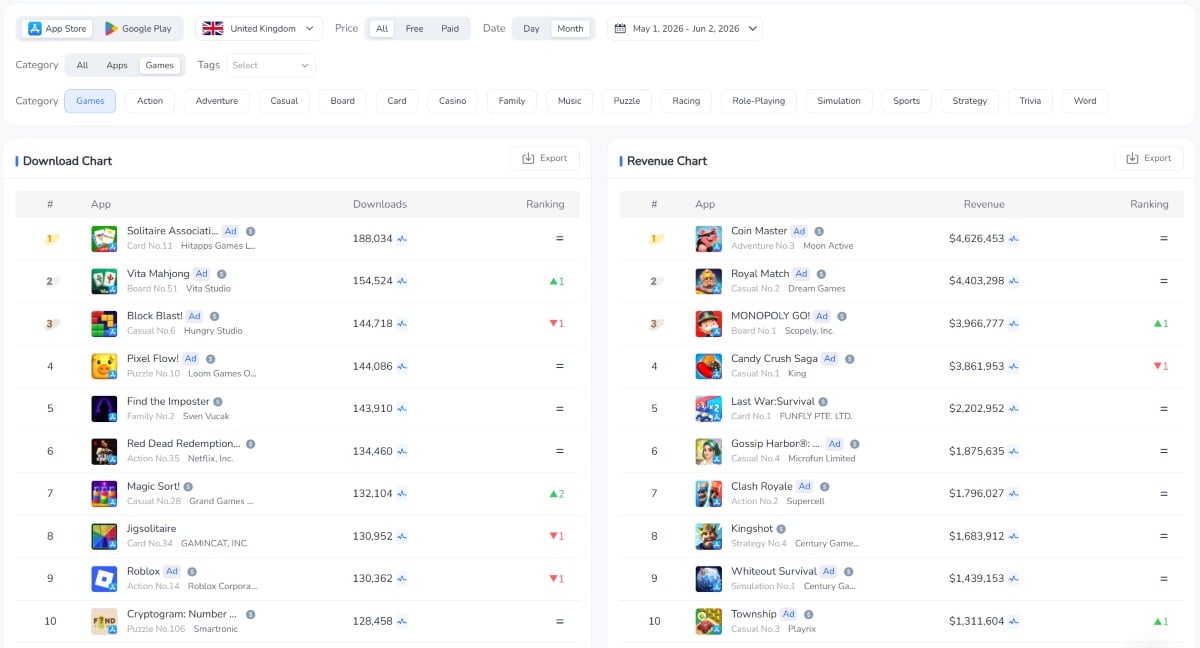

According to Intel Market Research, the United Kingdom alone commands a 28% share of regional market value - making it the single most critical European market for revenue-focused developers. Western Europe overall is described as "the undisputed leader" driven by high 5G penetration, near-universal smartphone adoption, and a consumer base with strong willingness to spend on in-app purchases.

UK mobile games market analytics — Game Download / Revenue data | Source from FoxData app marketing revenue report May, 2026

European studios have historically dominated specific genres that drive strong lifetime value (LTV). The region's genre leadership spans the full spectrum from hyper-casual to hardcore, creating a diversified revenue base that insulates the ecosystem from single-genre downturns:

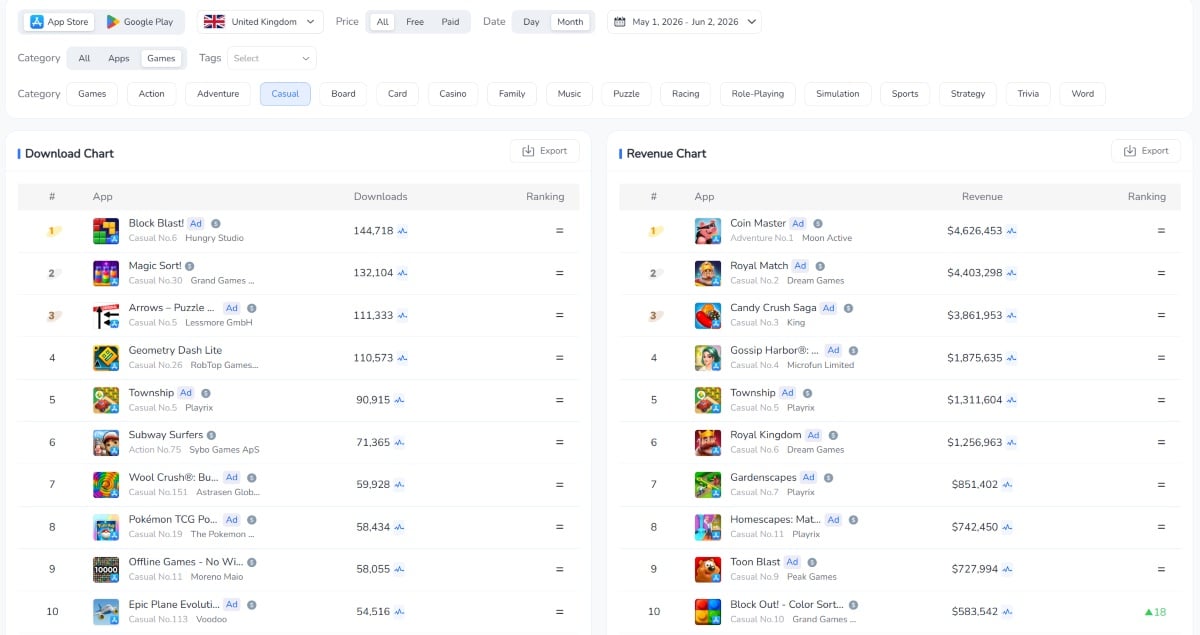

- Casual & Hyper-casual - European studios like Playrix (Estonia) and Voodoo (France) define the global casual meta. Hyper-casual titles remain the dominant download driver across European app stores, with ad-based monetization creating a steady revenue floor.

- Strategy & 4X - Finnish powerhouse Supercell (Clash of Clans, Clash Royale, Brawl Stars) continues to set the global standard. European strategy titles consistently occupy top-10 grossing positions across both App Store and Google Play.

- Puzzle - High retention, strong in-app purchase (IAP) monetization, and broad demographic appeal make this Europe's most reliable revenue genre.

- RPG & Mid-core - Growing segment with strong European publishing expertise, particularly from French and German studios. Poland's CD Projekt brings AAA-caliber RPG expertise to mobile, signaling the segment's maturation.

- Mobile Esports - Titles like PUBG Mobile and Clash Royale have established competitive scenes in Europe. Intel Market Research identifies organized tournaments and live-streaming partnerships as a "major frontier for growth" in the European market.

UK Casual & Hyper-casual game data | Source from FoxData app marketing revenue report May, 2026

📊 FoxData Perspective: Our genre-level data across European markets reveals a critical insight that aggregate reports often miss: genre revenue leadership varies significantly by country. Strategy titles dominate in Finland and Germany; puzzle games lead in the UK and France; hyper-casual drives volume in Southern and Eastern Europe. This fragmentation means that a pan-European launch strategy without country-level genre intelligence will systematically misallocate UA budgets. Developers using FoxData's free ASO tools can benchmark genre performance at the individual country level before committing to localization investment.

The economic data provides the credibility that enterprise-level conversations need. If you're pitching investors, partners, or co-development deals in Europe, €5.89 billion in GVA - projected to reach €6.17 billion by 2028 - is a conversation-starter that reframes mobile gaming from "entertainment product" to "strategic industry." The fact that mobile gaming accounts for 55% of all video games revenue globally adds further weight: mobile is no longer the side bet; it is the main event.

European markets are linguistically fragmented. The EU alone has 24 official languages, and app store ranking algorithms reward localized metadata, screenshots, and user reviews in each locale. A one-size-fits-all English approach will consistently underperform — especially given that 300 million Europeans play mobile games across dozens of linguistic communities.

📊 FoxData Insight: Our ASO & ASA agency data solutions are specifically designed to help developers track keyword performance across multiple European locales simultaneously - giving you the competitive intelligence to optimize metadata for German, French, Spanish, Italian, and other EU markets without guesswork. In our platform data, titles that localize for 5+ European languages consistently outperform English-only competitors by 2-4x in category ranking within those markets.

The jobs supported by European mobile gaming aren't concentrated at a handful of top-tier publishers. Spanning over 1,000 studios, the employment base includes:

• Ad tech and UA agencies running campaigns for mobile games

• Analytics providers helping studios understand player behavior

• Infrastructure companies providing cloud, CDN, and backend services

• QA studios, localization agencies, and IP licensing firms

This ecosystem creates B2B growth opportunities for tooling and services companies serving European mobile game studios - and it signals that the talent pool for mobile gaming is deep enough to sustain long-term expansion.

If the industry's policy advocacy succeeds, European developers may gain access to:

• R&D tax credits applicable to game development investment

• EU digital infrastructure grants reducing cloud hosting costs

• Talent visa frameworks making it easier to hire globally into European studios

For studios modeling 3-5 year financial projections, these policy variables are worth building into scenario planning. The European Commission's increasing engagement with the sector suggests that mobile gaming is moving from "tolerated" to "cultivated" in the policy framework.

The €7.53 billion in revenue that European studios generated came from global audiences - meaning European developers are competing with North American, Asian, and increasingly Middle Eastern studios for the same players. Winning globally requires understanding market-by-market dynamics at a granular level.

Key competitive dynamics from our platform data:

• Retention-focused monetization has overtaken pure acquisition spend as the primary growth lever since late 2025

• User acquisition costs in key Western European territories now frequently exceed €5 per install - making organic discovery through ASO a critical cost-containment strategy

• Cloud gaming services are growing at 45% and AI implementation in game development at 52%, per Intel Market Research - both trends that will reshape competitive dynamics by lowering technical barriers to high-fidelity mobile experiences

📊 FoxData Perspective: The convergence of 5G rollout (now covering 70%+ of the European population), cloud gaming growth, and AI-driven personalization means that the technical moat around high-production-value mobile games is shrinking. The new competitive barrier is data intelligence - understanding which markets, genres, and keyword landscapes offer the most efficient path to sustainable revenue. Our gaming app marketing analytics provide market-by-market visibility that replaces intuition with evidence.

Before entering or expanding in any European market, you need reliable competitive benchmarking data. This includes:

• Download and revenue estimates for your category and competitors

• Keyword ranking data across targeted locales

• Rating and review sentiment across app stores

• Update frequency and feature launch patterns of top competitors

FoxData's mobile game analytics solutions provide all of this in a single dashboard, with coverage across both the Apple App Store and Google Play Store in European markets.

For European markets specifically, ASO localization is where the highest ROI tends to live - because most international studios underinvest here. With 24 official EU languages and culturally distinct app store behavior across markets, localization is not a "nice-to-have" - it is the primary growth lever.

Key localization elements:

• Title and subtitle keyword optimization per locale

• Culturally adapted screenshots and preview videos

• Localized descriptions that match in-app experience

• Active review response in local languages (signals quality to both users and the algorithm)

Our free ASO tools can help you start keyword research across European markets at no cost - identify the gaps your competitors haven't closed.

European market success isn't measured at the continental level — it's measured by individual market performance. The KPIs that matter:

| KPI | Why It Matters in Europe |

|---|---|

| Category ranking by country | Ranking in DE vs. FR vs. ES can vary dramatically — Finland's top strategy title may rank #50+ in Spain |

| Keyword visibility score by locale | Each language market has different search behavior and keyword competition intensity |

| Conversion rate (store page to install) | Cultural preferences affect creative performance; what converts in Sweden may not in Italy |

| Review score by market | User expectations vary; negative reviews often cluster locally due to localization gaps |

| Revenue per install by market | ARPU varies 3-5x between Northern and Southern Europe — UA budget allocation must reflect this |

FoxData's app analytics and ASO performance metrics research tools give you this granularity without requiring you to build custom data pipelines.

For larger studios, agencies, and analytics teams that need to integrate market data into proprietary dashboards or BI systems, programmatic data access becomes essential.

📊 FoxData Insight: Our App Data API provides structured access to app store data - rankings, reviews, keyword performance, and more - enabling you to build automated monitoring systems for European market performance at scale. With 1,000+ studios competing across Europe and the market projected to reach USD 28.4 billion by 2030 (per Intel Market Research), manual data collection is no longer viable for serious competitors.

It's worth being analytically honest about what the economic impact figures do and don't capture:

What the Data Captures Well:

✅ Direct revenue generated by European-headquartered mobile game companies

✅ Employment multiplier effects through supply chain spending

✅ Broad economic contribution to European GDP

What the Data Likely Understates:

⚠️ Consumer surplus - the value players get beyond what they pay

⚠️ Cross-industry spillover - mobile gaming's role in driving smartphone adoption, mobile payment infrastructure, and 5G investment justification

⚠️ Informal economy contributions - content creators, streamers, and community managers who derive income from mobile gaming ecosystems without being formal employees

⚠️ Non-EU European markets - UK post-Brexit, Norway, Switzerland, and Turkey are significant mobile markets not fully captured in EU-focused economic contribution framing

What the Data Strategically Omits:

The Nordicity study is advocacy-oriented - commissioned by industry stakeholders with a policy agenda. That's not a criticism; it's context. The figures are credible and defensible, but structured to make the strongest possible case for favorable policy treatment. Developers should treat the data as a reliable floor estimate rather than a precise measurement.

📊 FoxData Perspective: While aggregate economic impact studies are valuable for policy advocacy, they don't replace the operational intelligence developers need to compete. The gap between "the European market is €5.89 billion" and "my puzzle game should target Germany first, with keyword strategy X" is bridged by platform-level data - the kind our tools provide at the individual app, category, and keyword level. The Nordicity report tells you the size of the ocean; FoxData's ASO tools tell you where the fish are.

The fact that Agence France-Presse (AFP) - one of the world's three major global news agencies - distributed coverage of this economic impact data signals that the story has moved beyond trade press. When a global wire service treats mobile gaming economic data as mainstream business news, it reflects genuine institutional recognition of the sector's scale.

The combination of AFP distribution, significant industry press pickup, and substantial LinkedIn engagement suggests this data will be referenced in policy discussions at the European Commission level. The framing is deliberate: helping policymakers understand the economic value of the mobile gaming ecosystem - and by extension, why it deserves strategic investment rather than regulatory indifference.

For developers and publishers: This is a moment to engage with industry associations, contribute to policy consultations, and make your voice heard alongside the larger players who are already doing so. The regulatory framework being shaped now — on R&D credits, talent mobility, and digital infrastructure - will define the competitive landscape for the next decade.

The economic impact data does something important: it quantifies what the mobile gaming industry has long known intuitively - that mobile games are a serious economic force in Europe, not a frivolous entertainment category. With 300 million players, 63,000 jobs, and a €5.89 billion contribution to the European economy - on a trajectory toward €6.17 billion by 2028 - the sector has earned its seat at the policy table.

For the studios and publishers competing in this market, the strategic implications are clear:

• European expansion is a data-driven game - market intelligence is the prerequisite, not an afterthought. The difference between Finland's €1.4 billion ecosystem and emerging Central European markets isn't just revenue; it's competitive dynamics, UA costs, and monetization profiles that demand granular analysis.

• ASO localization is your highest-ROI lever in a linguistically fragmented market serving 300 million players across two dozen languages. Titles that invest in multi-locale optimization consistently outperform those that don't.

• Policy tailwinds are real - track regulatory developments that could reshape your cost structure, from R&D credits to talent mobility frameworks.

• The competitive bar is rising - with the market projected to reach USD 28.4 billion by 2030 and AI/cloud technologies accelerating at 45-52% growth rates, European studios are serious global players. Competing against them requires serious tooling.

Whether you're a studio based in Berlin targeting the US market, or a US publisher looking to localize for Western Europe, the tools you use to understand and optimize your app store presence will define your competitive position.

📊 Start with data. Start with FoxData. From free ASO tools for initial market exploration to full-suite gaming analytics for scaling studios, FoxData provides the app store intelligence you need to compete in Europe's €5.89 billion mobile games market — and beyond.

All content, layout and frame code of all FoxData blog sections belong to the original content and technical team, all reproduction and references need to indicate the source and link in the obvious position, otherwise legal responsibility will be pursued.

Sources: Nordicity / Mobile Matters: The Impact of Mobile Games for Europe (June 2025); Intel Market Research - Europe Mobile Gaming Market Report; FoxData App Marketing Revenue Report (May 2026); Agence France-Presse (AFP); PocketGamer; GameReactor; WNHub.

© 2020-2026 FoxData. All Rights Reserved.