Explore More Possibilities for Your Business

Full-cycle scenario construction to meet your needs from App research, development, and release to operation.

Ready for your soaring growth

In 2024, the US mobile gaming market isn't just "growing"; it's evolving. Users are no longer just players; they are advertising touchpoints, content creators, and feedback anchors for algorithms.

With a GDP exceeding $29 trillion and annual mobile game revenue surpassing $23 billion, the download charts are a battleground for viral potential, while the revenue charts showcase algorithmic stability.

A single "Harder than you think" on TikTok, or a version update from Supercell, can shift the momentum of the entire overseas ecosystem. This is a multi-variable game, intricately woven with monetization models, creative narratives, behavioral psychology, and social amplification.

This analysis systematically breaks down the user behavior logic, monetization model formulas, channel distribution weights, and content topic trends in the US mobile gaming market, providing a "practical analysis framework" suitable for market validation.

In the first quarter of 2024, the US GDP approached $7 trillion, with a growth of 3.1%; the second quarter saw a GDP of $7.29 trillion, with an actual growth of 3%.

The third quarter's GDP further expanded to $7.365 trillion, with an actual growth of 2.5%. The fourth quarter saw a breakthrough, reaching $7.5 trillion—preliminary estimates place it at $7.55 trillion, a 2.8% increase compared to the same period last year, after adjusting for price changes in goods and services.

For the entire year of 2024, the US economy reached a record high of $29.2 trillion. Compared to the previous year, the actual growth, after removing inflation, was 2.9%, continuing to be at the upper end of the current economic development cycle. The nominal growth rate, without adjusting for inflation, was 5.3%.

As of January 2023, the U.S. boasts approximately 311 million internet users, with around 246 million active on social media platforms. Projections indicate continued growth in social media user numbers from 2024 to 2028, with an estimated 331 million users by 2028.

User base expansion is evident through rising penetration rates. From 2019 to 2028, the social network user penetration rate in the U.S. is forecast to steadily increase, reaching 95.71% by 2028. Notably, a significant proportion of Gen Z users spend over four hours daily on social media.

The number of social media users in the United States is projected to continue its upward trajectory, with an anticipated increase of 26 million users (+8.55%) between 2024 and 2029. Following nine consecutive years of growth, the social media user base is expected to reach 330.07 million users, peaking in 2029. This sustained growth underscores the enduring relevance of social media platforms.

As of March 2025, Facebook dominates the U.S. social media landscape, accounting for 56% of all social media website visits, solidifying its position as the leading platform. While other platforms enjoy significant popularity, their share of visits across desktop, mobile, and tablet devices is comparatively smaller. Pinterest ranks second, capturing 16.73% of all U.S. social media website visits, followed by X (formerly Twitter) at 11.73%.

According to FoxData data, the U.S. mobile game revenue reached $23.3 billion in 2023, contributing 30% of the global total. Following a decline in 2022 due to the end of the pandemic, U.S. mobile game revenue rebounded, with a 5.7% quarter-over-quarter increase in Q3 2023, signaling a return to growth.

In Q1 2024, the U.S. mobile game market continued its upward trajectory, with revenue increasing by 15% year-over-year, exceeding $6.4 billion.

2024, the number of mobile game downloads in the U.S. is expected to remain consistent with 2023. Hyper-casual, simulation, and action games are projected to maintain their positions as top download categories. The U.S. remains the highest-grossing market for mobile games globally, with in-app purchase revenue showing steady growth.

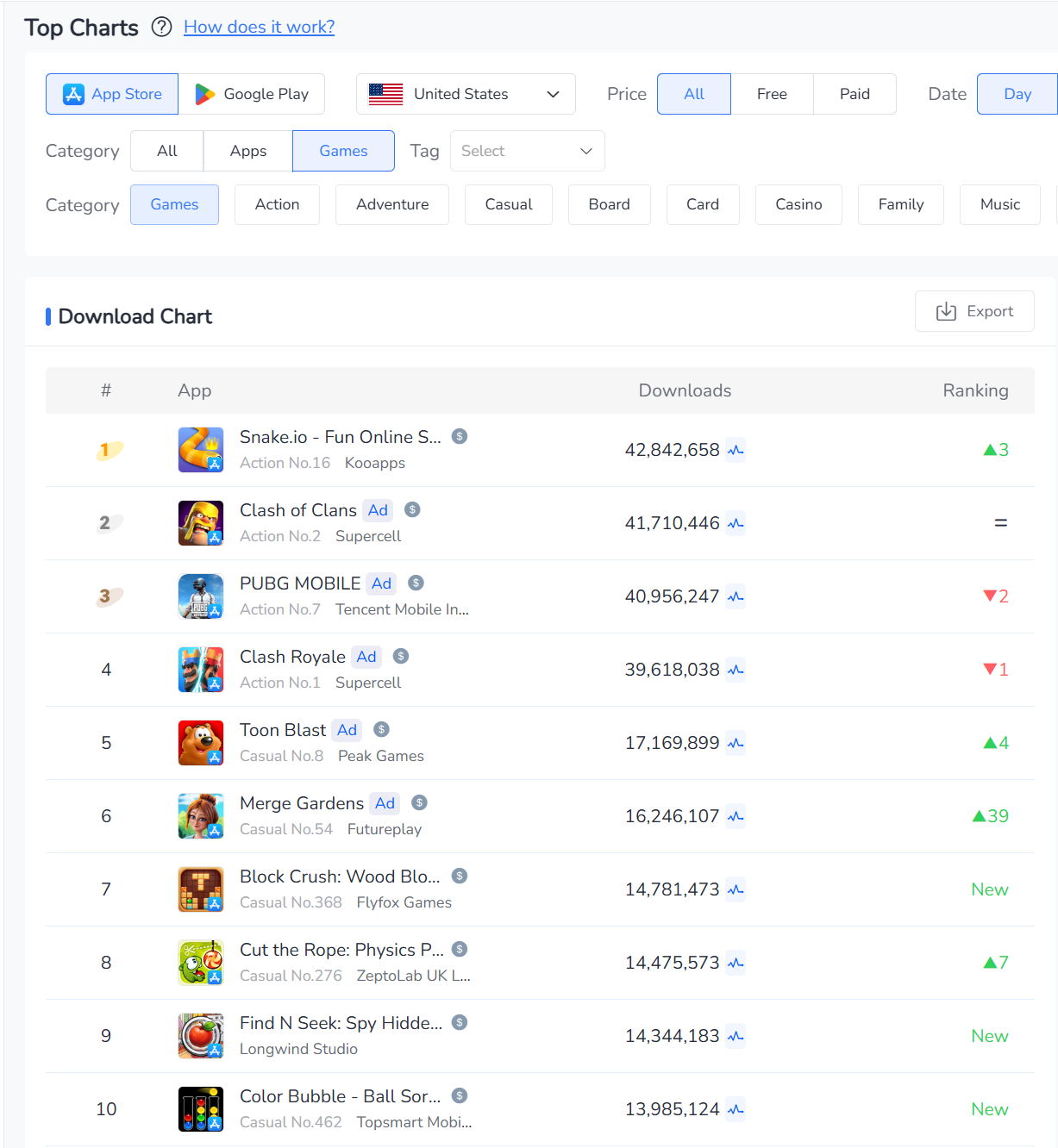

Download Chart

Analyzing the charts, the U.S. mobile gaming market in 2024 continues to be dominated by light casual games and classic, strong IP products in terms of new user acquisition.

Seven out of the top 10 downloaded games belong to the light casual or puzzle game categories, which have low barriers to entry. For example:

Snake.io, a minimalist multiplayer arena game, has attracted a large number of young users due to its low network load and instant competitive feel.

Puzzle and merge games like Cut the Rope, Merge Gardens, and Block Crush also demonstrate the market's strong demand for stress-relieving, relaxing, and fragmented time experiences.

Trend Insights: U.S. mobile game users are increasingly favoring games with short cycles, low learning costs, and high replayability, which are suitable for commuting, waiting, and other fragmented scenarios.

For example, Clash of Clans and Clash Royale by Supercell, as well as PUBG Mobile, are top products in the war, strategy, and competitive categories that have been operating for many years. Supported by continuous operation and optimized content update mechanisms, they have extremely strong user retention and re-propagation effects.

Strategy Framework: These products have established highly structured PvP systems, alliance mechanisms, and seasonal cycle mechanisms, forming a sustainable player return loop, which is a model of both user acquisition and retention.

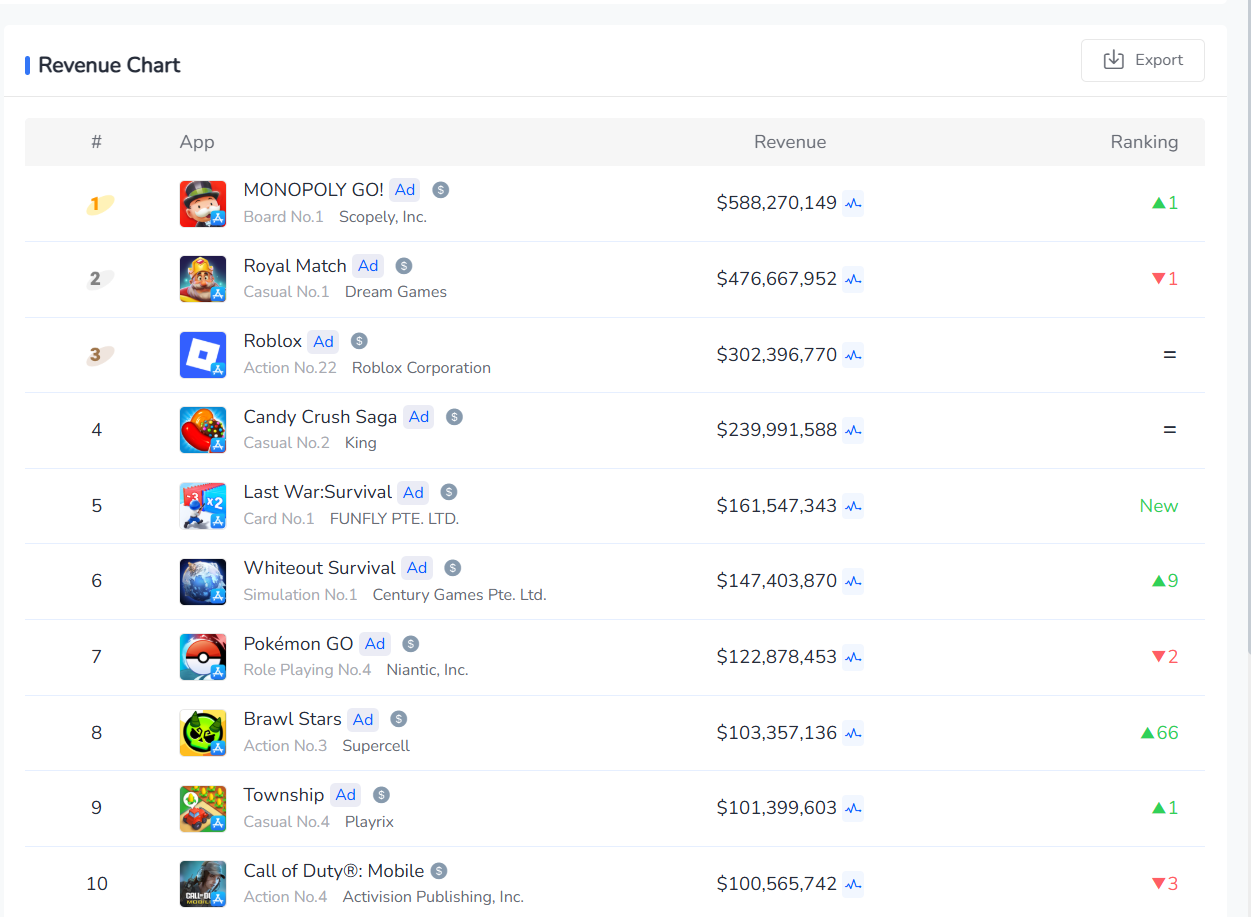

Revenue Chart

Unlike the trend towards lighter games on the download charts, the top 10 on the revenue charts showcase the monetization power of games with deep gameplay design, social loops, and content updates.

MONOPOLY GO! leads the pack, integrating a "social + collection + card" fusion system with board game mechanics. It enhances user social interaction and stickiness through friend gifting and stock dividends, strengthening the monetization path of in-game currency.

Classic match-3 games like Royal Match and Candy Crush continuously optimize their level economic models, coupled with time pressure and auxiliary props to build "pay-at-the-checkpoint" scenarios, achieving psychological-based conversions.

Analysis Conclusion: These games drive irrational user payment decisions through behavioral psychology mechanisms (such as the limited opportunity effect and goal-setting theory), which is one of the core logics of the current IAP model operation.

Roblox, as a UGC social platform, bases its profitability on the game creator ecosystem + virtual economic system. The Robux system forms an effective closed loop within the platform, and its business model transcends the boundaries of traditional games.

This type of product can provide a high degree of content creation freedom, satisfying the personalized expression and community belonging of "Generation Y" and "Generation Z" users, enabling them to have high payment potential even with a small amount of traffic activation.

The strategy + survival mobile games Whiteout Survival and Last War: Survival performed strongly for the first time, attributed to their deep integration with the preferences of European and American players, such as resource scheduling, confrontation systems, and construction mechanisms.

The simulation management game Township demonstrates a stable profit model with content expandability and a strong loop system, that is, extending the life cycle through the "drag time for money" logic.

U.S. players demonstrate a high acceptance of IP-based products and a strong willingness to pay. IP products can generate revenue through in-app purchases, advertising, and other methods. For instance, "Marvel Future Fight" has achieved substantial revenue by selling virtual items and skins, showcasing the commercial potential of IP games in the U.S. market. In terms of theme selection, science fiction, adventure, and magic themes are highly attractive due to their rich imagination and expressive power.

U.S. users are more inclined to accept creative and fun advertisements. They have a higher acceptance of local cultural elements. Incorporating localized elements such as "sexy beauties" and "gangster bosses" in advertisements can effectively attract player attention. Besides mainstream media like Facebook, Instagram, YouTube, and X, local super mobile apps like Twitch should not be overlooked.

In the first half of 2024, mobile game publishers invested over $650 million in digital advertising on popular platforms such as Facebook, Instagram, YouTube, and TikTok in the U.S. market. Strategy and RPG mobile games accounted for 35% and 28% of the advertising expenditure, respectively.

During this period, in-app purchase revenue for strategy mobile games in the U.S. market reached $2 billion, with an advertising ROI of 9.3. RPG mobile games generated nearly $1.2 billion, with an advertising ROI exceeding 7.

YouTube is the primary advertising channel for strategy and RPG mid-to-heavy mobile games in the U.S. market. In the first half of 2024, YouTube accounted for over 60% of the advertising expenditure for both strategy and RPG mobile games in the U.S. market.

Light mobile games in the U.S. market favor platforms like AppLovin, while YouTube has a higher SOV (Share of Voice) for mid-to-heavy mobile games.

In the US mobile gaming market, puzzle game ad SOV (Share of Voice) reached 34%, 40%, 37%, and 37% on platforms like AdMob, AppLovin, Mintegral, and Unity, respectively. Top advertisers in the puzzle game category include "Royal Match" and "Match Factory!".

Board game titles, such as "MONOPOLY GO!", exhibit a more even distribution of ad spend across various platforms, with an SOV of approximately 15% on AdMob, Apple Search Ads, AppLovin, Unity, and Facebook.

On YouTube, RPG and strategy games hold an SOV of 26% and 43%, respectively. Strategy games also show a preference for advertising on TikTok and Meta platforms.

Launched in April 2023 by Scopely, the board game title "MONOPOLY GO!" has seen continuous growth in in-app purchase revenue, driven by its adaptation and innovation of the classic Monopoly gameplay, along with significant ad spend. By October 2023, the game had surpassed $200 million in monthly revenue, securing its position as the top-grossing mobile game worldwide.

According to FoxData, as of June 2024, "MONOPOLY GO!" has spent $100 million on digital advertising in the U.S. market, generating a cumulative in-app purchase revenue of $2.2 billion, resulting in an impressive advertising ROI of 22.

In Q2 2024, Scopely's "MONOPOLY GO!" continued its advertising campaigns, leading the Share of Voice (SOV) for mobile game advertising across multiple platforms, including AdMob, Apple Search Ads, AppLovin, and Liftoff.

"Match Factory!", a 3D puzzle game by Peak Games, saw a significant increase in advertising SOV on AdMob and AppLovin platforms, ranking second and third respectively on these platforms in Q2 2024.

As mobile gaming penetration continues to rise, its surrounding content (such as guides, short videos, live streams, fan fiction, etc.) is no longer limited to the core player circle, but has become the mainstream dissemination material in the broad social media ecosystem.

Especially on short video platforms such as TikTok, YouTube Shorts, and Instagram Reels, this content is simple in structure, compact in rhythm, and highly reusable, making it easy to achieve viral growth, becoming an indispensable traffic port in brand marketing and product going global.

According to Google Trends (H1 2024), U.S. users searching for gaming content are no longer solely focused on game titles. Instead, they are increasingly concentrating on:

This search trend indicates that content consumption is shifting from "passive gameplay reception" to "player-driven exploration." In other words, searches with an action-oriented intent are increasing, providing more content marketing entry points for businesses.

Creative trend statistics from the TikTok Creative Center (Q1-Q2 2024) show that the most popular gaming ad keywords in the U.S. primarily include:

motion/Interest-Driven Phrases:

hallenge/Interaction-Driven Phrases:

Call to Action Phrases:

The aforementioned copy shares three key characteristics: Relatability, Challenge-Oriented, and an Urgent CTA, perfectly aligning with the impulsive, experimental behavior of TikTok's youthful user base. Data indicates that ads employing a "challenge + benefit" structure see 26%-43% higher engagement rates compared to straightforward presentations.

According to FoxData data, 48% of Gen Z users express interest in a game or product due to UGC on TikTok, rather than official ads.

This interest-based recommendation algorithm significantly reduces the cold-start costs for brands. Collaborating with live-streaming influencers, meme creators, or gaming content creators has become a core strategy for brands expanding overseas.

👁🗨FoxData's Exclusive Insights:

If this report has sparked some ideas, now is the perfect time to validate the value of our tools 🛠️.

🔍 Product trends, user analysis, creative monitoring, channel SOV, ROI calculations... The full FoxData product suite is now available, ready for immediate trial:

👉 Click to visit the product page and start your data-driven growth journey

© 2020-2026 FoxData. All Rights Reserved.